Executive Summary

India has undertaken its most sweeping overhaul of direct tax law in over six decades.

The Income Tax Act, 1961 — amended nearly 65 times with more than 4,000 changes across six decades — has been replaced by the Income Tax Act, 2025, effective April 1, 2026. This is not a tax hike.

Tax rates and slabs remain unchanged. But for HR professionals, payroll teams, and every salaried employee in India, the practical implications are significant, immediate, and demand urgent action.

This article provides an exhaustive, reference-grade breakdown of every change that matters — from restructured TDS sections and renamed forms, to expanded metro city HRA lists and the concurrent wage-code reform that is reshaping India's salary architecture.

Most importantly, it equips HR teams with actionable frameworks to guide employees through this transition, optimise their tax outcomes, and ensure the organisation is fully compliant.

2026 Tax Regime Optimization Engine

Calculate the exact break-even matrix point to choose which regimen fits for you and advise structural salary adjustments.

Verdict

New Regime Wins

Saves ₹12,500

New Regime Tax

₹0

Zero Proofs Required

Old Regime Tax

₹0

Deductions: ₹0

Part 1: Understanding the New Law — The Big Picture

1.1 Why India Replaced a 65-Year-Old Tax Law

The Income Tax Act, 1961 was a product of a different era. Over six decades, it was amended nearly 65 times through annual Finance Acts and 19 separate Taxation Laws Amendment Bills, accumulating more than 4,000 amendments.

By the time it was repealed, it had swelled to 819 sections across 47 chapters, totalling over 5.12 lakh words — a figure Finance Minister Nirmala Sitharaman publicly described as a 'maze.'

Source: Income Tax Department (incometax.gov.in) FAQs on the new Act; PRS Legislative Research analysis of the Income Tax (No. 2) Bill, 2025Three structural problems had compounded over time. The extensive amendment history made the law fragmented and internally inconsistent. Numerous exemptions and deductions over the decades had eroded the tax base and fuelled litigation. And the law's traditional 'legalese' — long sentences, provisos within provisos — made it effectively inaccessible to the average taxpayer.

1.2 What the New Act Actually Does

The Income Tax Act, 2025 (passed as the Income Tax (No. 2) Bill, 2025 by both Houses of Parliament in the monsoon session of 2025) does not change tax rates or tax policy. What it does is present the same tax policy in a dramatically restructured format.

Source: PRS Legislative Research — 'The Income-Tax (No.2) Bill, 2025'; Income Tax Department official FAQ| Parameter | Income Tax Act, 1961 | Income Tax Act, 2025 |

|---|---|---|

| Total Sections | 819 | 536 |

| Total Chapters | 47 | 23 |

| Schedules | Scattered | 16 consolidated schedules |

| Word Count | ~5.12 lakh words | Substantially reduced |

| Effective Date | April 1, 1962 | April 1, 2026 |

| Tax Year Concept | Previous Year + Assessment Year (separate) | Single 'Tax Year' framework |

| New Taxes Introduced | None Specified | None |

| Tax Rates Changed | Annual Fluctuations | No |

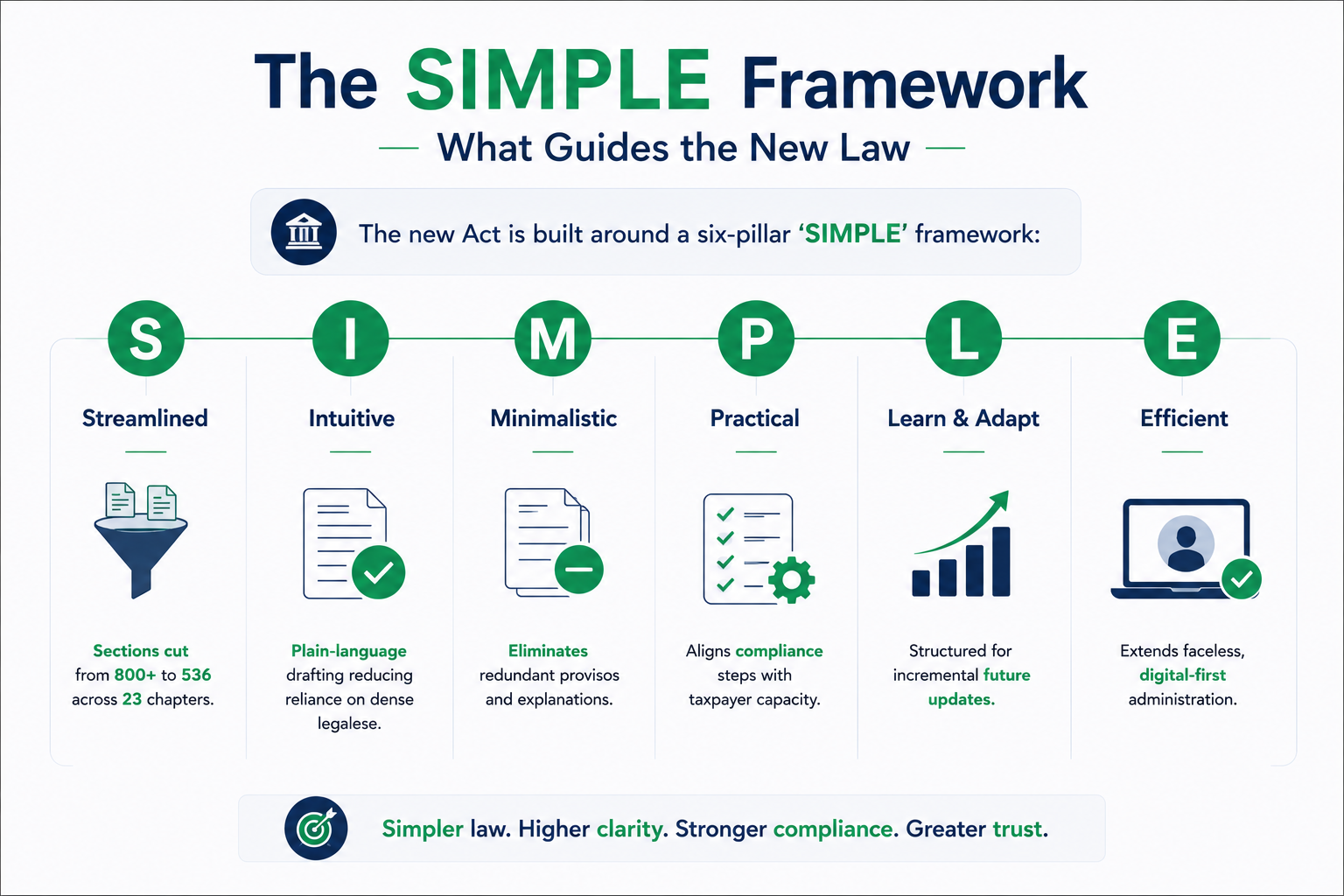

1.3 The SIMPLE Framework — What Guides the New Law

The new Act is built around a six-pillar 'SIMPLE' framework:

Streamlined (sections cut from 800+ to 536 across 23 chapters), Intuitive (plain-language drafting reducing reliance on dense legalese), Minimalistic (eliminates redundant provisos and explanations), Practical (aligns compliance steps with taxpayer capacity), Learn & Adapt (structured for incremental future updates), and Efficient (extends faceless, digital-first administration).

Source: Ujjivan SFB — 'New Income Tax Bill: Everything You Need to Know'; PIB Press Release on the Act1.4 The Critical Transition: What Law Applies When

This is perhaps the single most operationally confusing aspect for HR teams. Both the old and new Acts run in parallel for a transitional period.

Salary paid up to March 31, 2026: Governed by the Income Tax Act, 1961 (old law). TDS references old Section 192.

Salary paid from April 1, 2026 onwards: Governed by the Income Tax Act, 2025 (new law). TDS references new Section 392(1).

The governing law is determined by the date of payment, not the period of salary. So March 2026 salary paid on April 30, 2026 falls under the new Act. This is not merely academic — it affects section references, form numbers, and TDS calculation methodology.

Source: Income Tax Department FAQ on TDS transition; Upstox analysis — 'New TDS Rules for Salary from April 2026'📌 HR Action Item

Ensure payroll systems are updated to reference Section 392(1) for all salary payments made on or after April 1, 2026. Any continuation of Section 192 references will generate validation errors on the income tax portal.

Part 2: How the New Law Affects Employee Salaries

2.1 Tax Slabs and Rates — What Has NOT Changed

It is essential to lead with this: the new law does not change income tax slabs or rates. The same rates that applied in FY 2025-26 under Section 115BAC (new regime) continue to apply in Tax Year 2026-27 under the Income Tax Act, 2025. Employees should not expect higher or lower taxes purely because of the new Act.

Source: ClearTax 'Income Tax Slabs FY 2025-26'; Omni HR — 'India's Income Tax Act 2025 & Income Tax Rules 2026'Current Tax Slabs (New Regime — FY 2025-26 / Tax Year 2026-27)

| Annual Income (₹) | Tax Rate |

|---|---|

| Up to ₹4,00,000 | 0% (Nil) |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Additionally, a Section 87A rebate of ₹60,000 makes income up to ₹12 lakh effectively tax-free under the new regime. For salaried employees claiming the standard deduction of ₹75,000, effective tax-free income extends to ₹12.75 lakh.

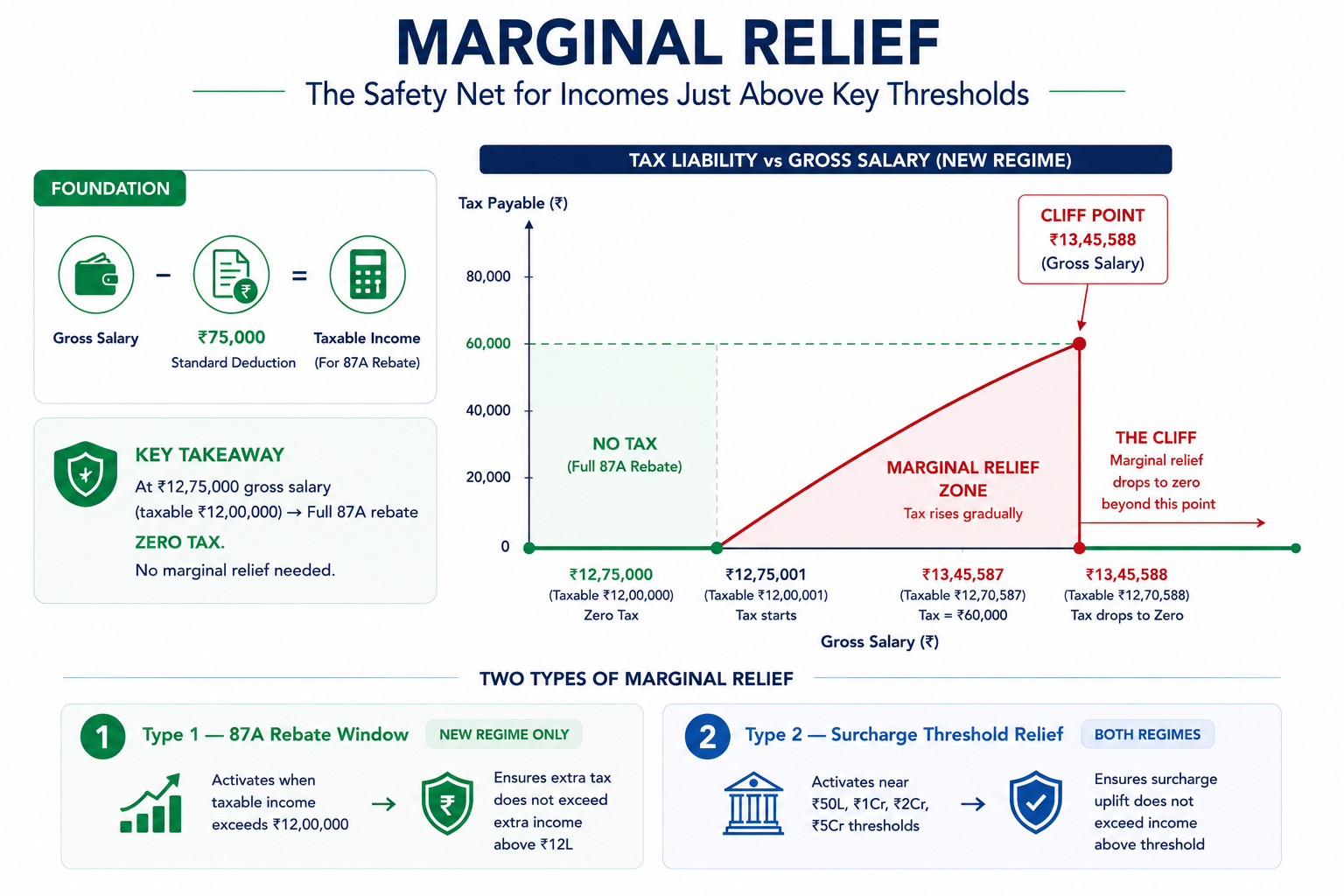

Source: ClearTax; Bajaj Finserv; Axis Max Life Insurance — Income Tax Slab analysis FY 2025-262.2 Marginal Relief — The Safety Net for Incomes Just Above Key Thresholds

First: Getting the Foundations Right — Standard Deduction vs. Taxable Income

Before understanding marginal relief, it is essential to be precise about two figures that HR payroll teams frequently conflate: gross salary and taxable income. They are not the same, and confusing them leads to incorrect TDS calculations.

- Gross Salary: What the employee earns before any deduction (e.g., Rs.13,50,000)

- Taxable Income: Gross salary minus the standard deduction of Rs.75,000 (e.g., Rs.13,50,000 - Rs.75,000 = Rs.12,75,000)

- Section 87A rebate applies to TAXABLE INCOME — not gross salary

A salaried employee earning a GROSS salary of Rs.12,75,000 has a TAXABLE INCOME of Rs.12,00,000 (after the Rs.75,000 standard deduction). Since taxable income is exactly Rs.12 lakh, the full Section 87A rebate of Rs.60,000 applies, and the tax payable is ZERO. No marginal relief is needed or applicable in this case.

This is the Finance Minister's stated intent: 'no income tax payable up to income of Rs.12 lakh... This limit will be Rs.12.75 lakh for salaried taxpayers, due to standard deduction of Rs.75,000.'

Source: PIB Press Release — Budget 2025 Finance Minister's statement; ClearTax — 'Income Tax Slabs FY 2025-26'; Ujjivan SFB — 'Marginal Tax Relief FY 2025-26'📌 Key Distinction for Payroll Teams: Marginal relief for salaried employees applies when GROSS SALARY exceeds Rs.12,75,000 (not Rs.12,00,000). At exactly Rs.12,75,000 gross, the employee pays ZERO tax. Marginal relief only becomes relevant for gross salaries from Rs.12,75,001 upwards (taxable income Rs.12,00,001+). Many payroll errors arise from applying this window to the wrong income figure.

Two Types of Marginal Relief — Both Matter for HR

- Type 1 — Section 87A Window (New Regime only): Applies when TAXABLE income is between Rs.12,00,001 and Rs.12,75,000. For salaried employees, this corresponds to GROSS salary between Rs.12,75,001 and Rs.13,50,000.

- Type 2 — Surcharge Threshold Relief (Both regimes): Applies when income marginally crosses surcharge thresholds of Rs.50 lakh, Rs.1 crore, Rs.2 crore, or Rs.5 crore.

Type 1: The Marginal Relief Window — Worked Examples (Salaried Employees)

The formula: Final tax payable = the amount by which TAXABLE INCOME exceeds Rs.12 lakh. Marginal Relief = Total tax computed on taxable income, minus that excess amount.

The table below shows the correct calculation using GROSS salary and TAXABLE income (after Rs.75,000 standard deduction) separately — because HR payroll teams work with gross salary figures:

| Gross Salary | Taxable Income (after Rs.75K std. deduction) | Tax Before Relief | Excess Over Rs.12L | Marginal Relief | Final Tax |

|---|---|---|---|---|---|

| Rs.12,75,000 | Rs.12,00,000 | Rs.60,000 (full rebate) | Nil | N/A — full rebate applies | Rs.0 (ZERO) |

| Rs.12,85,000 | Rs.12,10,000 | Rs.61,500 | Rs.10,000 | Rs.51,500 | Rs.10,000 |

| Rs.13,25,000 | Rs.12,50,000 | Rs.67,500 | Rs.50,000 | Rs.17,500 | Rs.50,000 |

| Rs.13,45,588 | Rs.12,70,588 | Rs.70,588 | Rs.70,588 | Rs.0 | Rs.70,588 |

| Rs.13,50,000 | Rs.12,75,000 | Rs.71,250 | Rs.75,000 | No relief — beyond window | Rs.71,250 + 4% cess |

| Rs.14,00,000 | Rs.13,25,000 | Rs.78,750 | Rs.1,25,000 | No relief — beyond window | Rs.78,750 + 4% cess |

📌 The Real Tax Cliff — and Where It Sits: The true tax cliff happens exactly at a Gross Salary of Rs.13,45,588. An employee earning Rs.13,45,588 gross pays Rs.70,588 in tax. Beyond this precise point, the marginal relief window closes, and at Rs.13,50,000 gross the standard slab tax applies seamlessly. Payroll teams must be precise about this calculation framework.

Live Marginal Relief Simulator

Move the slider to see the step-by-step mathematical degradation of the relief window up to the exact threshold cliff.

Cliff Reached: Marginal Relief has dropped to Zero. Full tax slabs now apply.

Taxable Income

₹12,00,000

Excess over ₹12L

₹0

Base Tax Computed

₹67,500

Marginal Relief

₹0

Final Tax Payable

(Excludes 4% cess)

₹0

Who Qualifies for Type 1 Marginal Relief?

- Resident individual taxpayers under the NEW tax regime only — not available under the old tax regime

- TAXABLE income strictly between Rs.12,00,001 and Rs.12,70,588 (for salaried employees, this means GROSS salary between Rs.12,75,001 and Rs.13,45,588 approximately)

- Both salaried and non-salaried individuals qualify (note: non-salaried individuals have no standard deduction, so their marginal relief window is Rs.12,00,001 to Rs.12,70,588 of gross income directly)

- NOT available to NRIs, HUFs, companies, or LLP/partnership firms

Type 2: Surcharge Marginal Relief (Senior/High-Income Employees — Both Regimes)

For executives earning above Rs.50 lakh, surcharge is levied on computed income tax. This is available under both old and new regimes. Surcharge rates:

| Total Income Range | Surcharge Rate (New Regime) | Surcharge Rate (Old Regime) |

|---|---|---|

| Up to Rs.50 lakh | Nil | Nil |

| Rs.50 lakh to Rs.1 crore | 10% | 10% |

| Rs.1 crore to Rs.2 crore | 15% | 15% |

| Rs.2 crore to Rs.5 crore | 25% | 25% |

| Above Rs.5 crore | 25% (capped) | 37% |

Without marginal relief, an employee earning Rs.51 lakh would pay Rs.14,76,750 in tax (including 10% surcharge), while one earning exactly Rs.50 lakh pays Rs.13,12,500. That extra Rs.1 lakh of income causes an additional Rs.1,64,250 in tax — far exceeding the extra income earned. Marginal relief caps the additional tax at Rs.1,00,000 (the actual excess income). The relief amount is Rs.64,250, reducing total tax to Rs.14,12,500.

Source: Canara HSBC Life; Tax2Win — 'Surcharge on Income Tax and Marginal Relief'Surcharge marginal relief formula: Relief = (Tax including surcharge on actual income) minus (Tax at threshold) minus (Excess income over threshold). If this figure is positive, it is deducted from total tax liability.

Source: Zoho Payroll Academy — 'Surcharge on Income Tax and Marginal Relief'📌 HR Action Item: For senior employees earning Rs.50 lakh+, TDS must account for both the surcharge and applicable marginal relief. Payroll software that does not handle this automatically can result in over-deduction (employee dissatisfaction) or under-deduction (1.5%/month interest liability on the employer). Verify your system handles surcharge marginal relief automatically before processing payroll for high-income executives.

Is Marginal Relief Applied Automatically During ITR Filing?

Yes — when employees file their ITR online, the e-filing portal automatically computes both surcharge and applicable marginal relief based on the income declared. Employees do not need to calculate or claim it manually. However, this only corrects the annual filing. For monthly TDS accuracy throughout the year, the employer's payroll system must project annual income correctly and apply marginal relief so deductions are calibrated from April itself — preventing a large refund or demand at the time of filing.

Source: Axis Max Life Insurance — 'Marginal Relief in Income Tax: Meaning and Calculation FY 2025-26'2.3 Standard Deduction — A Meaningful Relief

The standard deduction available to salaried employees and pensioners has been increased from ₹50,000 to ₹75,000 under the new tax regime (under the old regime, it remains ₹50,000). This is a flat, automatic deduction that requires no proof or documentation — it is applied directly to gross salary to arrive at taxable income.

Source: ClearTax 'Income Tax Slabs FY 2025-26'; HDFC Life — 'Income Tax Slab Rates FY 2025-26'Practical impact: A salaried employee earning ₹12.75 lakh gross per annum pays zero income tax under the new regime — the ₹75,000 standard deduction brings taxable income to ₹12 lakh, and the Section 87A rebate eliminates the remaining liability entirely.

Source: IndiaFirst Life — 'New Income Tax Bill 2025: Key Changes and Impact'2.3 The HRA Metro City Expansion — A Significant Win for Tech Employees

One of the most impactful changes for India's rapidly growing metros is the expansion of the 'metro city' definition for HRA (House Rent Allowance) exemption purposes. Under the old law (Rule 2A of Income Tax Rules 1962), only four cities qualified for the higher 50% HRA exemption: Delhi, Mumbai, Kolkata, and Chennai. Employees in Bangalore, Hyderabad, Pune, and Ahmedabad — cities with rental costs often comparable to or exceeding traditional metros — were limited to a 40% exemption.

Source: Housing.com — 'Which are the metro cities in India for HRA calculation'; Deccan Herald — 'Income Tax Rules 2026 Explained'Under the Income Tax Rules, 2026, effective April 1, 2026, the list expands to eight cities: Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Pune, and Ahmedabad. All eight now qualify for the 50% HRA exemption.

Source: Omni HR — 'India's Income Tax Act 2025 & Income Tax Rules 2026'; Zoho Payroll Academy — 'New Income Tax Act 2025'Important caveat: This benefit applies under the old tax regime only. The HRA exemption is not available under the new tax regime. However, employees of Bengaluru, Hyderabad, Pune, and Ahmedabad who choose to remain on the old regime now benefit from a materially improved exemption.

| City | Old HRA Exemption Rate | New HRA Exemption Rate (from April 2026) |

|---|---|---|

| Delhi | 50% | 50% (unchanged) |

| Mumbai | 50% | 50% (unchanged) |

| Kolkata | 50% | 50% (unchanged) |

| Chennai | 50% | 50% (unchanged) |

| Bengaluru | 40% | 50% (upgraded) |

| Hyderabad | 40% | 50% (upgraded) |

| Pune | 40% | 50% (upgraded) |

| Ahmedabad | 40% | 50% (upgraded) |

| All other cities | 40% | 40% (unchanged) |

📌 HR Action Item: Employees in Bengaluru, Hyderabad, Pune, and Ahmedabad who are on the old tax regime must resubmit Form 124 (the new name for old Form 12BB) with updated HRA calculations applying 50% (not 40%). Payroll systems must be updated before the first April 2026 payroll run.

2.4 Perquisites — Tighter Valuation, New Inclusions

Under the Income Tax Rules, 2026, perquisite valuation norms have been overhauled to be 'rule-prescribed' — meaning the taxable value of non-cash benefits is now determined by specific rules rather than employer discretion. This has direct payroll implications.

Source: India Briefing — 'Year Zero: Why India's Income-Tax Rules 2026 Demand an Urgent Payroll Audit'; Zoho Payroll AcademyCompany Car Perquisites

For employer-provided motor cars used partly for official and partly for personal purposes, the taxable monthly perquisite value depends on engine capacity and who bears running costs:

- EV / Car up to 1.6 litre engine (employer bears costs): ₹5,000/month taxable (+ ₹3,000/month if chauffeur provided)

- Car above 1.6 litre engine (employer bears costs): Higher taxable value

- Employee bears running costs: ₹2,000/month taxable (+ ₹3,000/month if chauffeur provided)

Notably, electric vehicles (EVs) are now explicitly included and treated at par with cars up to 1.6 litre engine capacity — a recognition of the growing EV adoption in corporate fleets.

Source: Business Today — 'Simplified Income Tax Law from April 1'; Zoho Payroll Academy — 'New Income Tax Act 2025'Children's Education & Hostel Allowances

Exemption limits for children's education allowance have been revised upward to ₹3,000 per month per child (previously ₹100), and hostel expenditure allowance to ₹9,000 per month per child (previously ₹300), both limited to two children. These long-overdue revisions make these allowances meaningful in a modern cost environment.

Source: Zoho Payroll Academy — 'New Income Tax Act 2025: A Complete Guide'The HRA Family Landlord Rule

When an employee pays rent above ₹1 lakh annually to a family member (parent, spouse, or sibling), this must now be disclosed in Form 124 along with the landlord's PAN and declared relationship. Missing this disclosure invalidates the HRA claim entirely.

Source: Zoho Payroll Academy — 'New Income Tax Act 2025'📌 HR Action Item: Review your HRA declaration process. Employees who pay rent to family members must complete the relationship disclosure on Form 124. HR must proactively communicate this to avoid disqualified claims and TDS shortfalls.

2.5 NPS (National Pension System) — Continued Advantage

The National Pension System remains one of the most tax-efficient components of any salary structure, and this benefit is available under both regimes:

- Employer contributions to employee NPS Tier-I accounts are exempt up to 10% of salary (basic + DA) under the old regime, and up to 14% of salary under the new tax regime, subject to an overall cap of ₹7.5 lakh per year combined across employer contributions to PF, NPS, and superannuation funds.

- Employee's own additional NPS contributions up to ₹50,000 per year are deductible under Section 80CCD(1B) under the old tax regime — and this is over and above the ₹1.5 lakh Section 80C limit.

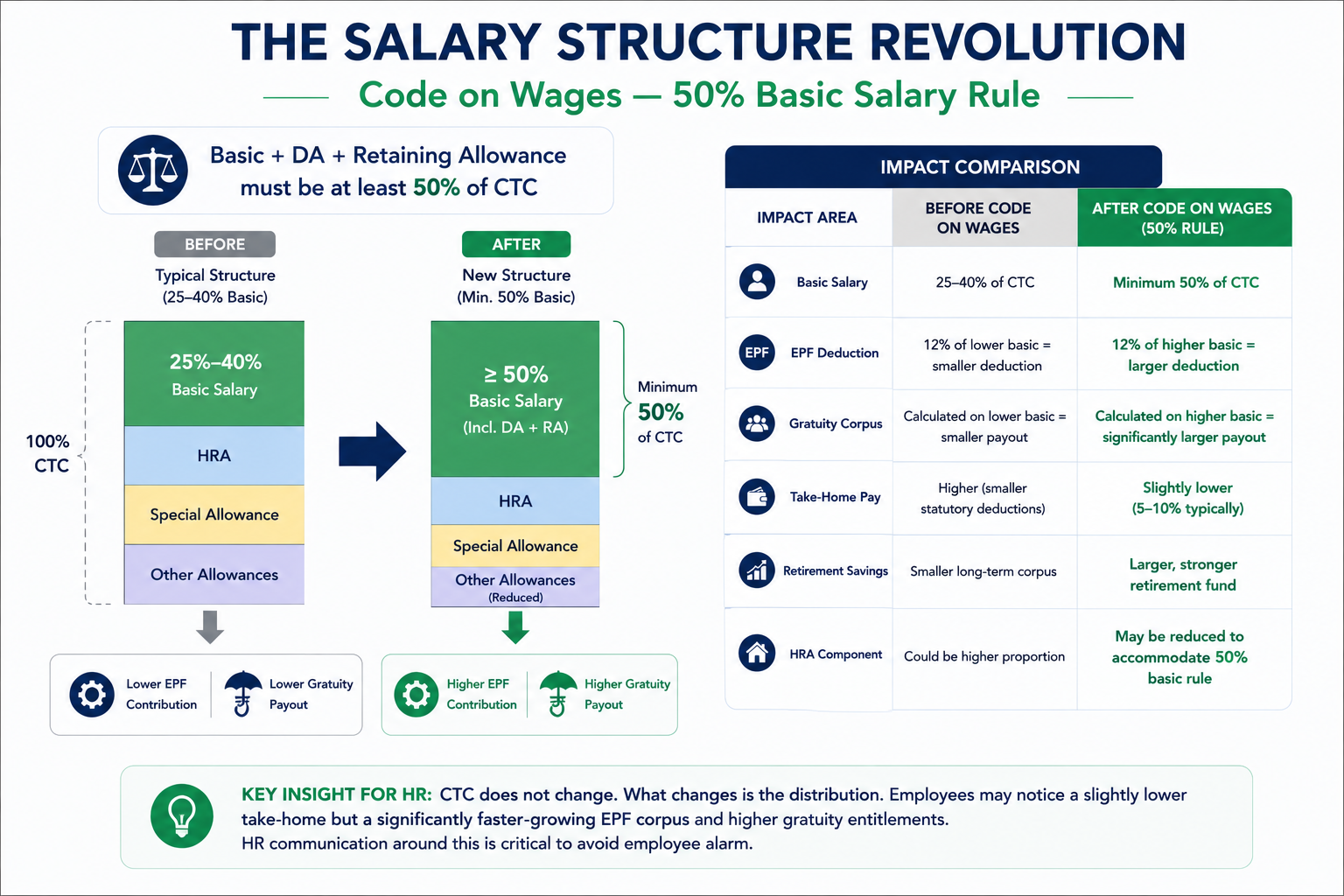

2.6 The Salary Structure Revolution: Code on Wages — 50% Basic Salary Rule

Running concurrent with the Income Tax Act, 2025 is the implementation of the Code on Wages, 2019. While these are separate pieces of legislation, their combined effect fundamentally reshapes salary structures across India.

The most significant change: basic salary, dearness allowance, and retaining allowance must together constitute at least 50% of an employee's total CTC.

Source: Wisecor Global — 'Salary Changes from April 2026'; Labour Law Reporter — EPF Act India; Zee Biz — 'Labour Codes 50% Wage Rule Explained'This is a significant departure from historical practice. For years, companies — particularly in the private sector — kept basic salary artificially low (often 25-40% of CTC) to minimize statutory contributions to EPF and gratuity. The new rule eliminates this practice.

Source: Wisecor Global; AccountX — 'New Labour Codes 2026: Payroll Compliance Guide'What Changes for Employees

| Impact Area | Before Code on Wages | After Code on Wages (50% Rule) |

|---|---|---|

| Basic Salary | 25-40% of CTC typically | Minimum 50% of CTC |

| EPF Deduction | 12% of lower basic = smaller deduction | 12% of higher basic = larger deduction |

| Gratuity Corpus | Calculated on lower basic = smaller payout | Calculated on higher basic = significantly larger payout |

| Take-Home Pay | Higher (smaller statutory deductions) | Slightly lower (5-10% typically) |

| Retirement Savings | Smaller long-term corpus | Larger, stronger retirement fund |

| HRA Component | Could be higher proportion | May be reduced to accommodate 50% basic rule |

📌 Key Insight for HR: CTC does not change. What changes is the distribution. Employees may notice a slightly lower take-home but a significantly faster-growing EPF corpus and higher gratuity entitlements. HR communication around this is critical to avoid employee alarm.

Part 3: The New Compliance Framework — Forms, TDS, and Filing

3.1 The Tax Year Concept — Eliminating the 'Assessment Year' Confusion

For decades, Indian employees struggled with the dual-year system: income earned in 'Financial Year 2025-26' was assessed in 'Assessment Year 2026-27.' This required constant mental translation. The Income Tax Act, 2025 eliminates this by introducing a single 'Tax Year' concept.

Income earned from April 1, 2026 to March 31, 2027 is simply called Tax Year 2026-27 — it is earned, filed, and assessed within the same labelled period.

Source: ClearTax — 'Income Tax Act 2025 — Key Changes'; The Peoples Board — 'Income Tax Act 2025: Key Changes for HR Teams'Note: The Tax Year still equals the Financial Year. The change is terminology and conceptual clarity — not how tax is calculated. But every piece of HR documentation, offer letters, salary slips, investment declarations, and employee communication must now use 'Tax Year' instead of 'Assessment Year.'

3.2 New Forms — What HR Must Issue

| Old Form | New Form | Purpose | Deadline |

|---|---|---|---|

| Form 16 | Form 130 | Annual TDS certificate for salaried employees | June 15 of following Tax Year |

| Form 12BB | Form 124 | Employee investment/rent declaration to employer | Start of Tax Year (April) |

| Form 24Q | Form 138 | Quarterly TDS return for salary (filed by employer) | Standard quarterly deadlines |

| Form 16A | Form 131 | TDS certificate for non-salary income | As applicable |

| Form 27D | Form 133 | TCS certificate | As applicable |

| Form 3CD | Form 26 | Tax audit report | Per audit filing deadline |

📌 Critical Compliance Alert: Issuing a document labelled 'Form 16' for Tax Year 2026-27 salary is technically non-compliant under the new law. The correct form is Form 130. Employees relying on Form 16 for ITR filing will face mismatches on the e-filing portal. HR must update all templates immediately.

3.3 New TDS Sections — The 192-Series is Retired

Under the Income Tax Act, 1961, TDS was governed by a sprawling series of 194-series sections (194C, 194J, 194I, etc.) plus Section 192 for salary. All of these have been retired. The new Act consolidates TDS into three parent sections:

- Section 392 — Salary TDS (replaces Section 192 and 192A)

- Section 393 — All other TDS (replaces 194C, 194J, 194I, 194H, 194A, 194D, 194DA, 194N, 194R, 194S, and all others)

- Section 394 — All TCS provisions

TDS rates themselves have not changed. What changed is the structural referencing. Any ERP system or payroll software still referencing 194C, 194J, etc. for April 2026 transactions will generate validation errors on the income tax portal.

3.4 The Investment Declaration Process — Updated References

Employees who choose the old tax regime must submit investment declarations (now Form 124, replacing Form 12BB) at the start of the Tax Year (April). Section references in these declarations have changed because the new Act reorganises provisions:

- Old Section 80C (₹1.5 lakh deduction): Now referenced as Schedule XV read with Section 123 of the Income Tax Act, 2025

- Old Section 80D (health insurance): Referenced under new section numbering

- Old Section 80CCD (NPS): Referenced under new section numbering

📌 HR Action Item: Update investment declaration templates (now Form 124) to reference new section numbers from the Income Tax Act, 2025. Employees submitting declarations with old section numbers may face confusion during ITR filing.

Part 4: The Old Regime vs. New Regime — A Strategic HR Decision

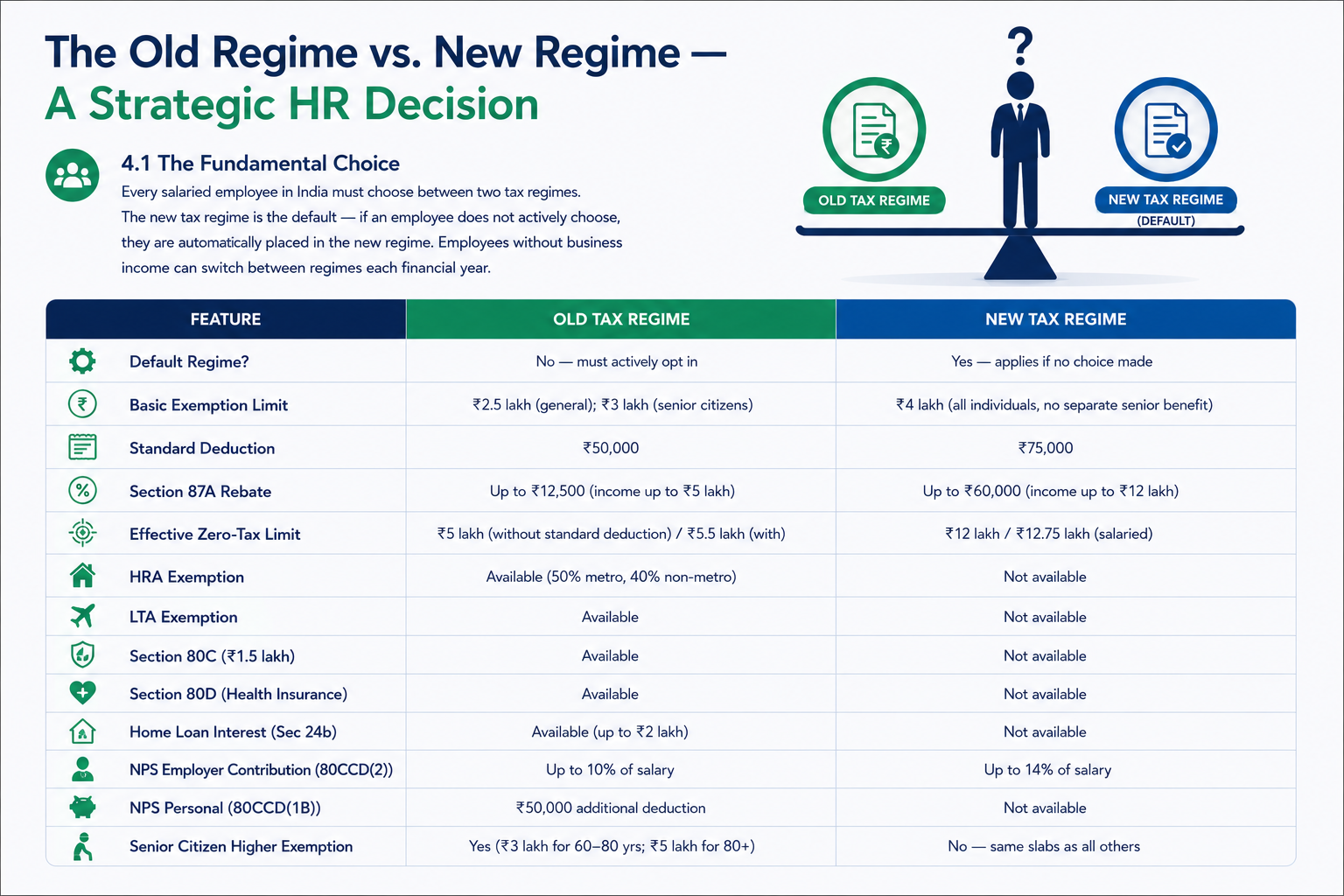

4.1 The Fundamental Choice

Every salaried employee in India must choose between two tax regimes. The new tax regime is the default — if an employee does not actively choose, they are automatically placed in the new regime. Employees without business income can switch between regimes each financial year.

Source: ClearTax 'Income Tax Slabs FY 2025-26'; HDFC Life — 'Income Tax Slab FY 2025-26'

| Feature | Old Tax Regime | New Tax Regime |

|---|---|---|

| Default Regime? | No — must actively opt in | Yes — applies if no choice made |

| Basic Exemption Limit | ₹2.5 lakh (general); ₹3 lakh (senior citizens) | ₹4 lakh (all individuals, no separate senior benefit) |

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 87A Rebate | Up to ₹12,500 (income up to ₹5 lakh) | Up to ₹60,000 (income up to ₹12 lakh) |

| Effective Zero-Tax Limit | ₹5 lakh (without standard deduction) / ₹5.5 lakh (with) | ₹12 lakh / ₹12.75 lakh (salaried) |

| HRA Exemption | Available (50% metro, 40% non-metro) | Not available |

| LTA Exemption | Available | Not available |

| Section 80C (₹1.5 lakh) | Available | Not available |

| Section 80D (Health Insurance) | Available | Not available |

| Home Loan Interest (Sec 24b) | Available (up to ₹2 lakh) | Not available |

| NPS Employer Contribution (80CCD(2)) | Up to 10% of salary | Up to 14% of salary |

| NPS Personal (80CCD(1B)) | ₹50,000 additional deduction | Not available |

| Senior Citizen Higher Exemption | Yes (₹3 lakh for 60-80 yrs; ₹5 lakh for 80+) | No — same slabs as all others |

4.2 Who Should Choose Which Regime — HR's Decision Framework

The break-even point where both regimes yield equal tax depends on income level and total deductions. Here is a practical framework HR advisors can use:

Typically Better Off with the NEW Regime

- Employees earning up to ₹12.75 lakh annually — zero tax obligation

- Employees with minimal deductions (no home loan, no large 80C investments, no significant HRA)

- Freshers and young employees who have not yet built an investment portfolio

- Employees living in company-provided accommodation (no HRA to claim)

- High earners above ₹24 lakh who prefer simplicity and don't have deductions exceeding ~₹8 lakh

Potentially Better Off with the OLD Regime

- Employees who can claim large HRA (especially now in expanded metro cities)

- Employees with home loans claiming ₹2 lakh interest deduction under Section 24b

- Employees maximising Section 80C (₹1.5 lakh) + 80D (₹25,000-₹50,000) + NPS 80CCD(1B) (₹50,000)

- Mid-range earners (₹12 lakh–₹24 lakh) with significant investments

Expert guidance: If total deductions (excluding standard deduction) exceed approximately ₹8 lakh, the old regime may yield better outcomes. Below ₹3.75 lakh in deductions, the new regime is almost always better.

Source: IndiaFilings — 'Old vs New Tax Regime 2025'; SBI General — 'Income Tax Slabs'; Futurex Solutions — 'TDS on Salary in India'Part 5: What HR Must Do — An Action Framework

5.1 Immediate Compliance Actions (Must Be Done Before First April Payroll)

- Update all payroll software and ERP systems to reference Section 392(1) for salary TDS, replacing old Section 192. Validate that the system rejects old section numbers for April 2026 transactions.

- Replace all references to Form 16 with Form 130, Form 12BB with Form 124, Form 24Q with Form 138 in all internal templates, HRMS, and payroll tools.

- Update HRA exemption city classifications in payroll — Bengaluru, Hyderabad, Pune, and Ahmedabad now qualify for 50% (not 40%) under the old regime.

- Collect fresh investment declarations from all employees using Form 124, with updated section references from the Income Tax Act, 2025.

- Review all perquisite valuations — especially company cars, ESOPs, accommodation, and food allowances — against the Income Tax Rules, 2026 before the first payroll run.

- Update all employee-facing documents (offer letters, salary slips, tax declarations) to use 'Tax Year' instead of 'Financial Year/Assessment Year.'

5.2 Salary Restructuring — Responding to the 50% Wage Rule

If your organisation has not already restructured salary to comply with the Code on Wages 50% basic salary rule, this must be a priority. Here is what HR needs to do:

- Audit all current salary structures — identify every employee whose basic pay + DA is below 50% of CTC.

- Recalculate EPF contributions for affected employees at the new higher basic.

- Revise employment contracts and offer letters to reflect the new structure.

- Update payroll software to automatically apply the new wage definition.

- Proactively communicate to employees: CTC is unchanged, but take-home may reduce slightly while EPF and gratuity grow. Frame this as a long-term retirement benefit, not a pay cut.

5.3 Employee Communication Strategy

The biggest risk in this transition is not compliance failure — it is employee alarm. Employees who see payslip changes without explanation will assume errors, misunderstand the law, or lose trust in HR. A proactive communication plan is essential.

Recommended Communication Timeline

| When | What to Communicate | Channel |

|---|---|---|

| April (Tax Year start) | New regime vs old regime choice; Form 124 deadline; what changes on payslip | Email + townhall + HR portal |

| April (first payslip) | Explanation of any payslip changes; standard deduction applied; new form names | Payslip note + email |

| June 15 | Form 130 issuance (replacing Form 16); how to use it for ITR filing | Email + download link |

| July–August | ITR filing support; deadline reminders; help sessions | Newsletter + HR helpdesk |

| January–March | Investment proof submission window; regime reconsideration opportunity | Reminder emails + 1-on-1 sessions for senior staff |

5.4 Helping Employees Optimise Tax Returns — A Practical HR Guide

For Employees Under the NEW Regime

- Ensure ₹75,000 standard deduction is applied automatically in payroll — no action needed from employee

- Encourage employer NPS contributions up to 14% of salary (Section 80CCD(2)) — the only major deduction available

- Help employees understand that the regime is optimal for simplicity and for incomes up to ₹12.75 lakh

- No investment proofs needed — ITR filing is simpler and faster

For Employees Under the OLD Regime

- Ensure Form 124 is submitted by April with complete HRA details (including landlord PAN if rent > ₹1 lakh/year) and relationship disclosure if paying rent to family

- Maximise Section 80C/Schedule XV investments (₹1.5 lakh): ELSS, PPF, EPF, life insurance premiums, NSC, home loan principal

- Encourage health insurance (Section 80D): ₹25,000 for self/family + ₹25,000 for parents (₹50,000 each if senior citizens)

- Advise NPS personal contributions of ₹50,000 (Section 80CCD(1B)) — additional deduction beyond 80C

- Ensure HRA is claimed with correct city classification — employees in Bengaluru, Hyderabad, Pune, Ahmedabad: update to 50%

- For home loan holders: claim ₹2 lakh interest deduction under Section 24b + principal under 80C

5.5 The HR Team's Regime Advisory Role

HR should not tell employees which regime to choose — that is a personal financial decision. But HR should ensure every employee has the information and tools to make the choice correctly. The People Matters framework recommends seven HR responsibilities in this context:

- Understand employee requirements at various life stages through focus groups and feedback

- Help employees understand both regimes and the implications of choosing each

- Work with payroll to update systems and tax calculators

- Design and offer flexible benefits where the organisation's policy permits

- Review existing programs based on employee preferences and utilisation

- Create awareness around overall financial wellness — not just tax saving

- Educate employees on the April deadline to express regime preference

📌 Best Practice: Run an annual April tax webinar where HR explains regime choices, walks through payslip changes, and gives employees a tax calculator session. Provide individual 15-minute advisory slots for employees with complex situations (home loans, ESOPs, family-member HRA).

Part 6: Special Situations HR Must Handle

6.1 ESOPs and Equity Compensation

Under the Income Tax Rules, 2026, ESOP perquisite valuation norms have been updated and brought under stricter 'rule-prescribed' valuations. Employers who under-value ESOPs in TDS calculations risk the 1.5% per month interest on shortfall — and the liability sits with the employer, not the employee. Senior management and expatriate compensation packages particularly warrant a full review.

Source: India Briefing — 'Year Zero: Why India's Income-Tax Rules 2026 Demand an Urgent Payroll Audit'6.2 Joining and Termination Bonuses

The Income Tax Act, 2025 explicitly includes joining bonuses and termination compensation within the scope of taxable salary. Any such payments made from April 1, 2026 onwards must be included in TDS calculations under Section 392.

Source: India Briefing — 'Year Zero'; Zoho Payroll Academy6.3 Senior Citizen Employees

One potential downside of the new regime for senior employees: under the old regime, senior citizens (60-80 years) benefited from a higher basic exemption limit of ₹3 lakh, and super senior citizens (above 80) from ₹5 lakh. The new regime has no such distinction — the same slabs apply to everyone. Senior employees who previously benefited from the old regime's higher exemption should carefully model their liability under both regimes.

Source: ClearTax 'Income Tax Slabs FY 2025-26'; Manipal Cigna — 'Income Tax Slabs New Regime'6.4 Virtual Digital Assets (Crypto)

The new Act formally recognises virtual digital assets (VDAs) — cryptocurrencies and tokens — within its statutory framework. VDAs are now explicitly included in the definition of 'undisclosed income' for search cases, and virtual digital spaces are subject to access during search and seizure. Taxation rates on VDAs themselves remain unchanged (30% flat).

Source: PRS Legislative Research — 'The Income-Tax (No.2) Bill, 2025'; ClearTax — 'Income Tax Act 2025 Key Changes'Part 7: Real-World Salary Examples

All calculations below use the FY 2025-26 slab rates. New regime: 0-4L @ 0%, 4-8L @ 5%, 8-12L @ 10%, 12-16L @ 15%, 16-20L @ 20%, 20-24L @ 25%, above 24L @ 30%. Old regime: 0-2.5L @ 0%, 2.5-5L @ 5%, 5-10L @ 20%, above 10L @ 30%. Plus 4% health & education cess on final tax in all cases.

Scenario A: ₹8 Lakh Annual Gross Salary (Entry-Level Engineer, Bengaluru)

Assumptions: Employee pays rent of ₹20,000/month in Bengaluru (now a 50% metro under new rules). HRA received = ₹1,20,000/year (assumed). 80C investments = ₹1,50,000. No home loan.

| Component | Old Regime | New Regime |

|---|---|---|

| Gross Salary | ₹8,00,000 | ₹8,00,000 |

| Less: Standard Deduction | ₹50,000 | ₹75,000 |

| Less: HRA Exemption (50% — Bengaluru now qualifies) | ₹1,20,000 (illustrative) | Not available |

| Less: 80C Deduction | ₹1,50,000 | Not available |

| Taxable Income | ₹4,80,000 | ₹7,25,000 |

| Tax on Taxable Income | ₹11,500 [0 on ₹2.5L + 5% on ₹2.3L] | ₹16,250 [0 on ₹4L + 5% on ₹3.25L] |

| Section 87A Rebate | ₹11,500 (full — income below ₹5L) | ₹16,250 (full — income below ₹12L) |

| Net Tax Payable (before cess) | ₹0 | ₹0 |

| 4% Health & Education Cess | ₹0 | ₹0 |

| TOTAL TAX PAYABLE | ₹0 | ₹0 |

| Verdict | Zero tax | Zero tax — and simpler to file (no proofs needed) |

Scenario B: ₹20 Lakh Annual Gross Salary (Mid-Level Manager, Mumbai)

Assumptions: Employee lives in rented accommodation in Mumbai and receives HRA of ₹2,40,000/year (illustrative). Has home loan, health insurance, and NPS investments. Old regime standard deduction = ₹50,000; new regime = ₹75,000.

| Component | Old Regime | New Regime |

|---|---|---|

| Gross Salary | ₹20,00,000 | ₹20,00,000 |

| Less: Standard Deduction | ₹50,000 | ₹75,000 |

| Less: HRA Exemption (50% Mumbai) | ₹2,40,000 | Not available |

| Less: 80C Deduction | ₹1,50,000 | Not available |

| Less: 80D Health Insurance | ₹25,000 | Not available |

| Less: Home Loan Interest (Sec 24b) | ₹2,00,000 | Not available |

| Less: NPS 80CCD(1B) | ₹50,000 | Not available |

| Taxable Income | ₹12,85,000 | ₹19,25,000 |

| Tax Calculation (slab-wise) | 0 on ₹2.5L + 5% on ₹2.5L (₹12,500) + 20% on ₹5L (₹1,00,000) + 30% on ₹2.85L (₹85,500) | 0 on ₹4L + 5% on ₹4L (₹20,000) + 10% on ₹4L (₹40,000) + 15% on ₹4L (₹60,000) + 20% on ₹3.25L (₹65,000) |

| Tax Before Cess | ₹1,98,000 | ₹1,85,000 |

| 4% Health & Education Cess | ₹7,920 | ₹7,400 |

| TOTAL TAX PAYABLE | ₹2,05,920 | ₹1,92,400 |

| Verdict | New regime is cheaper by ~₹13,500 even with all deductions | New regime wins in this case |

Note: This example illustrates that in many cases with moderate deductions, the new regime can still be cheaper. Employees should always model both regimes with their own actual deduction amounts — results vary significantly based on specific figures, especially if home loan interest or HRA is very high.

Source: Tax slab rates from ClearTax; old regime slab rates confirmed via HDFC Life and Tax Concept; calculation methodology per official Income Tax Act provisionsScenario C: ₹10 Lakh Gross Salary (New Regime — Zero Tax)

Gross salary ₹10,00,000. Less standard deduction ₹75,000. Taxable income = ₹9,25,000.

Tax: 0 on ₹4L + 5% on ₹4L (₹20,000) + 10% on ₹1.25L (₹12,500) = ₹32,500 before rebate.

Section 87A rebate = ₹32,500 (fully absorbed, as taxable income is below ₹12L). Net tax = ₹0.

A taxpayer earning ₹10 lakh annually under the new regime therefore has zero tax liability.

For context, under the old tax regime, an employee earning ₹10 Lakh gross who fully utilized Section 80C (₹1.5L) and had no other deductions would pay ₹75,400 in tax. The revised New Regime eliminates this entirely without requiring a single investment proof.

Part 8: Key Deadlines & HR Compliance Calendar

| Deadline | Action Required | Responsible Party |

|---|---|---|

| April 1, 2026 | New law effective — all systems must reference new sections and forms | HR + Payroll + IT |

| April (first week) | Collect Form 124 (investment declarations) from all employees | HR |

| April 30, 2026 | First payroll under Income Tax Act, 2025 — must use Section 392(1) | Payroll |

| May 31, 2026 | Q1 TDS return (Form 138) filing deadline | Finance / Payroll |

| June 15, 2026 | Issue Form 130 (replacing Form 16) to all employees for FY 2025-26 | HR / Payroll |

| July 31, 2026 | Employee ITR filing deadline (typically) | Employees — HR support |

| Oct–Nov 2026 | Advance tax calculation and deposit (second instalment) | Payroll + Finance |

| Jan–Mar 2027 | Investment proof submission window (old regime employees) | HR collects; employees submit |

References & Sources

All factual claims in this article are supported by the following primary and secondary sources:

| Source | Type | URL / Reference |

|---|---|---|

| "Income Tax Department, Govt. of India — Official FAQ on New Act" | Primary / Official | incometax.gov.in — 'Objective and Scope of the New Act' |

| "Income Tax Department — Income Tax Act, 2025 (full text)" | Primary / Official | incometaxindia.gov.in/income-tax-act-20251 |

| "CBDT — Gazette Notification, Income Tax Rules, 2026" | Primary / Official | "Notified March 20, 2026" |

| "PRS Legislative Research — 'The Income-Tax (No.2) Bill, 2025'" | Secondary / Legislative | prsindia.org |

| "PIB Press Release — 'Understanding the Income Tax Act, 2025'" | Primary / Official | pib.gov.in |

| ClearTax — Income Tax Slabs FY 2025-26 | Secondary / Financial | cleartax.in/s/income-tax-slabs |

| ClearTax — Income Tax Act 2025 Key Changes | Secondary / Financial | cleartax.in/s/income-tax-act-2025 |

| ClearTax — TDS and TCS Changes from April 2026 | Secondary / Financial | cleartax.in |

| Zoho Payroll Academy — 'New Income Tax Act 2025: A Complete Guide' | Secondary / HR/Payroll | zoho.com/in/payroll |

| The Peoples Board — 'Income Tax Act 2025: Key Changes for HR Teams' | Secondary / HR | thepeoplesboard.com |

| Omni HR — 'India's Income Tax Act 2025 & Income Tax Rules 2026' | Secondary / HR | omnihr.co |

| India Briefing — 'Year Zero: Why India's Income-Tax Rules 2026 Demand an Urgent Payroll Audit' | Secondary / Legal/HR | india-briefing.com |

| Business Today — 'New Tax Regime 2026: How Salary Components Will Tweak' | Secondary / News | businesstoday.in |

| "Business Today — 'New Labour Code 2025: Impact on Tax, PF, NPS'" | Secondary / News | businesstoday.in |

| Futurex Solutions — 'TDS Changes from April 2026' | Secondary / Compliance | futurexsolutions.com |

| AccountX — 'New Labour Codes 2026: Payroll Compliance Guide' | Secondary / HR | accountx.in |

| Wisecor Global — 'Salary Changes from April 2026' | Secondary / HR/Payroll | wisecorglobal.com |

| Futurex Solutions — 'New Salary Structure 2026' | Secondary / Compliance | futurexsolutions.com |

| IndiaFilings — 'Old vs New Tax Regime 2025' | Secondary / Financial | indiafilings.com |

| People Matters — 'A Guide to Choose Between Old and New Tax Regime' | Secondary / HR | peoplematters.in |

| Asanify — 'Comprehensive Guide to Employee Tax Optimization' | Secondary / HR/Finance | asanify.com |

| Bajaj Finserv — 'Income Tax Slabs FY 2025-26' | Secondary / Financial | bajajfinancier.in |

| HDFC Life — 'Income Tax Slab Rates FY 2025-26' | Secondary / Financial | hdfclife.com |

| IndiaFirst Life — 'New Income Tax Bill 2025' | Secondary / Financial | indiafirstlife.com |

| CompuTax — 'TDS Changes from April 2026' | Secondary / Tech/Compliance | computaxonline.com |

| Labour Law Reporter — EPF Act India | Secondary / Legal | labourlawreporter.com |

| LawChakra — 'Labour Codes 2025 Explained' | Secondary / Legal | lawchakra.in |

| Upstox — 'New TDS Rules for Salary from April 2026' | Secondary / Finance | upstox.com |

Disclaimer

This document is prepared for HR informational and educational purposes. It is not legal or tax advice. Individual tax situations vary — employees should consult a qualified Chartered Accountant for personalised guidance. All regulatory information is current as of May 2026.